These charts shows why you shouldn't retire in a down market

These charts shows why you shouldn't retire in a down market

When it comes to retirement, timing is everything. And for retirees, good timing doesn't just have to do with threading the needle on Social Security start dates or savvily initiating required minimum distributions (RMDs). It also has to do with understanding the markets. That's because retiring during a down market can have a long-term impact on the health and longevity of retirement savings.

This is related to what is known as sequence risk. It typically refers to the hazards posed by making early retirement withdrawals during a down market. Retirees who launch into retirement during a bear market, for example, may see that initiating drawdowns in a poor investment environment does major damage to their long-term savings.

After a stomach-sinking 2022 in which the S&P 500 fell nearly 20%, SmartAsset crunched the numbers to see how much starting retirement in a down year can impact long-term investment savings.

To uncover the long-term impacts of early down-market retirement withdrawals, SmartAsset looked back at two previous bear markets: 2001 and 2008. We examined what would have happened to the long-term savings of a retiree holding $1 million in an investment account at the start of a year in which stocks lost value – and whether waiting until markets recovered to retire improved the health of their long-term savings.

Here's a breakdown of the profiles for these aspiring retirees:

Retirement dates. The first two retirees in our analysis plan to retire in 2000. The second two plan to retire in 2008, the year of the Great Recession.

Drawdown rate. Each saver plans on a 4% drawdown rate, which will increase with the historical rate of inflation. We assume these accounts don't have required minimum distributions (RMDs) or mandated withdrawals.

Investment mix. The pre-retirees each maintain a portfolio of investments that is pegged 50% to the S&P 500 and 50% to the performance of a popular bond index mutual fund.

Different retirement dates. This is where our aspiring retirees differ. In each bear market, one retiree barrels ahead with retirement, beginning account withdrawals in a down year and locking in losses early. The other investor waits until the year when markets start to recover, retiring in a period when markets are on the upswing.

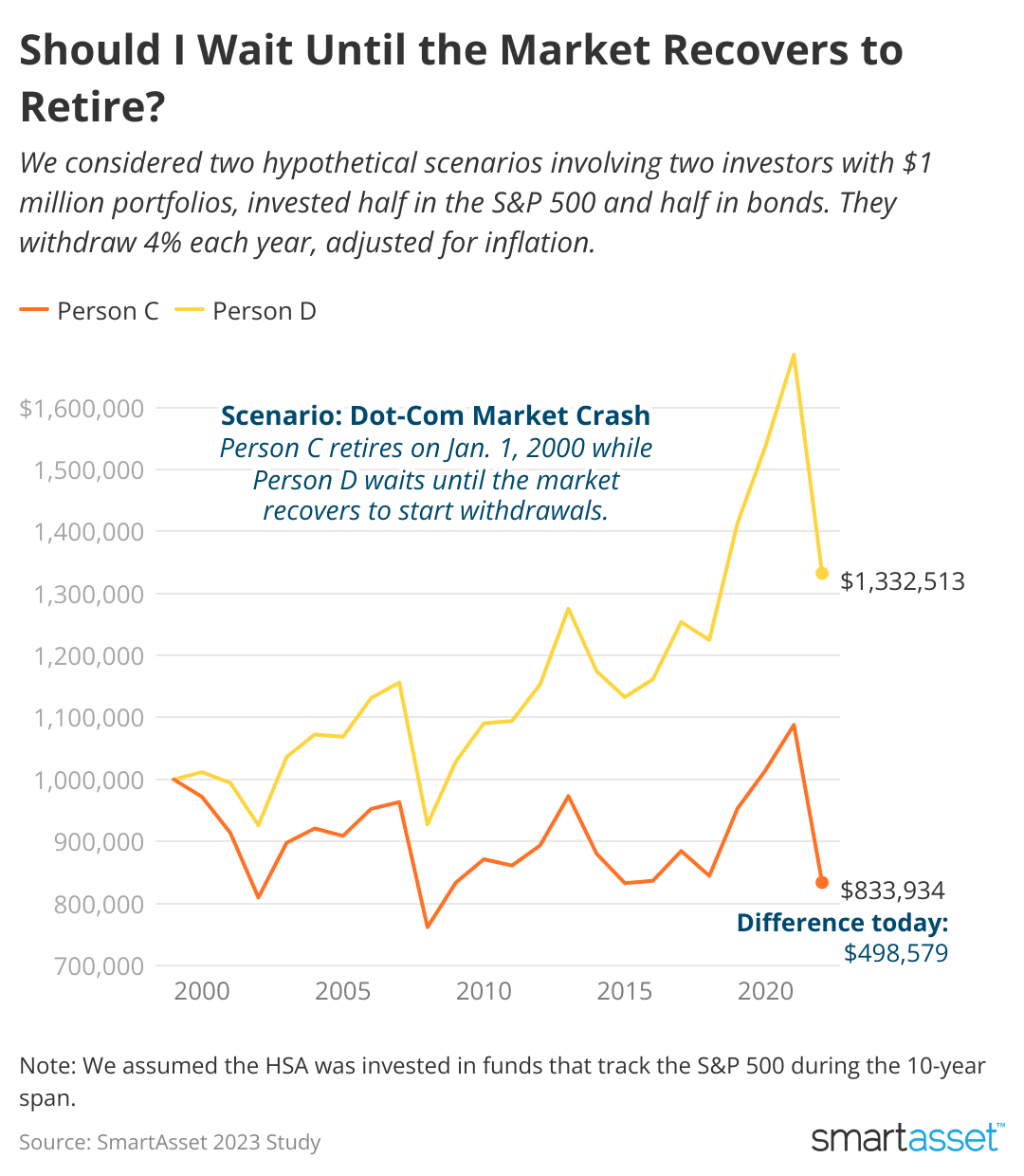

The 2001 bear market

Pre-retirees C and D both have $1 million saved at the beginning of the early-2000s bear market. Since they're retiring soon, their portfolios track a half-and-half mix of stocks and bonds.

But as markets start to plunge, Retiree D decides to delay retirement account withdrawals, choosing to work longer or perhaps live on cash savings for an additional three years. Her account still takes a beating throughout the bear market, but she doesn't lock in losses by making withdrawals. Today, her account is worth $1,332,513.

Retiree C, on the other hand, goes ahead as planned. She retires. Despite experiencing the same annual returns, rates of inflation and subsequent withdrawals, the difference is stark. Her account is worth $833,934.

Retiree D, who waited to start making withdrawals until the market recovered, has $498,579 more left in her retirement account today than Retiree C has. That's the difference a few years makes.

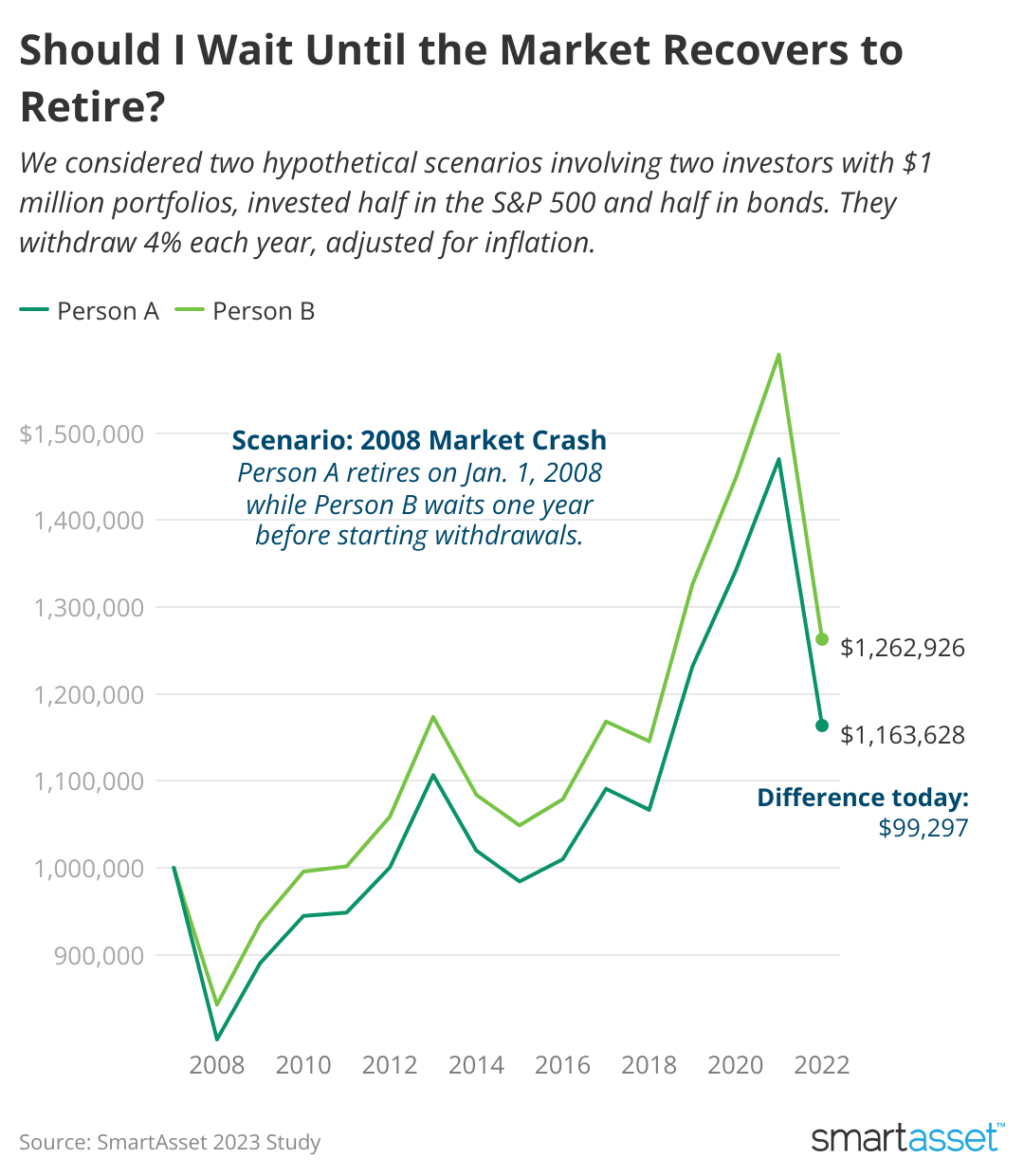

The 2008 bear market

The same two scenarios apply here. Retiree A doesn't wait to start making withdrawals on his accounts, choosing to initiate withdrawals in 2008 during a down market. His balance today: $1,163,628.

Retiree B waits just one additional year – when the markets have recovered. Her balance today is $1,262,926. The total difference between the two, after just one extra year of delayed withdrawals, is $99,297.

The Importance of Sequence Risk

For retirees staring down the barrel of a bear market, it may make sense to wait an additional year or two to start drawing down on retirement accounts.

Of course, hindsight is 20-20, and pinpointing an extended down market and recovery is impossible – and not advisable – for most retirees. Even still, if the wheels are already in motion on retirement, and markets are starting to tank, newbie retirees may be able to pivot quickly to reduce or avoid drawdowns. That can help them dodge the impact of poor early retirement returns on their savings.

Four common strategies to do so may include:

- Continuing to work, even on a part-time or consulting basis.

- Tapping short-term cash savings or other funding sources before withdrawing investments.

- Opting to reduce withdrawals – perhaps taking 2% in an early down year instead of the full 4%.

- Delaying big expenses such as vacations for another year or two to reduce or eliminate withdrawals.

No matter what strategies retirees use, reducing drawdowns in a bear market, especially early in retirement, can have a substantial impact on retirement longevity.

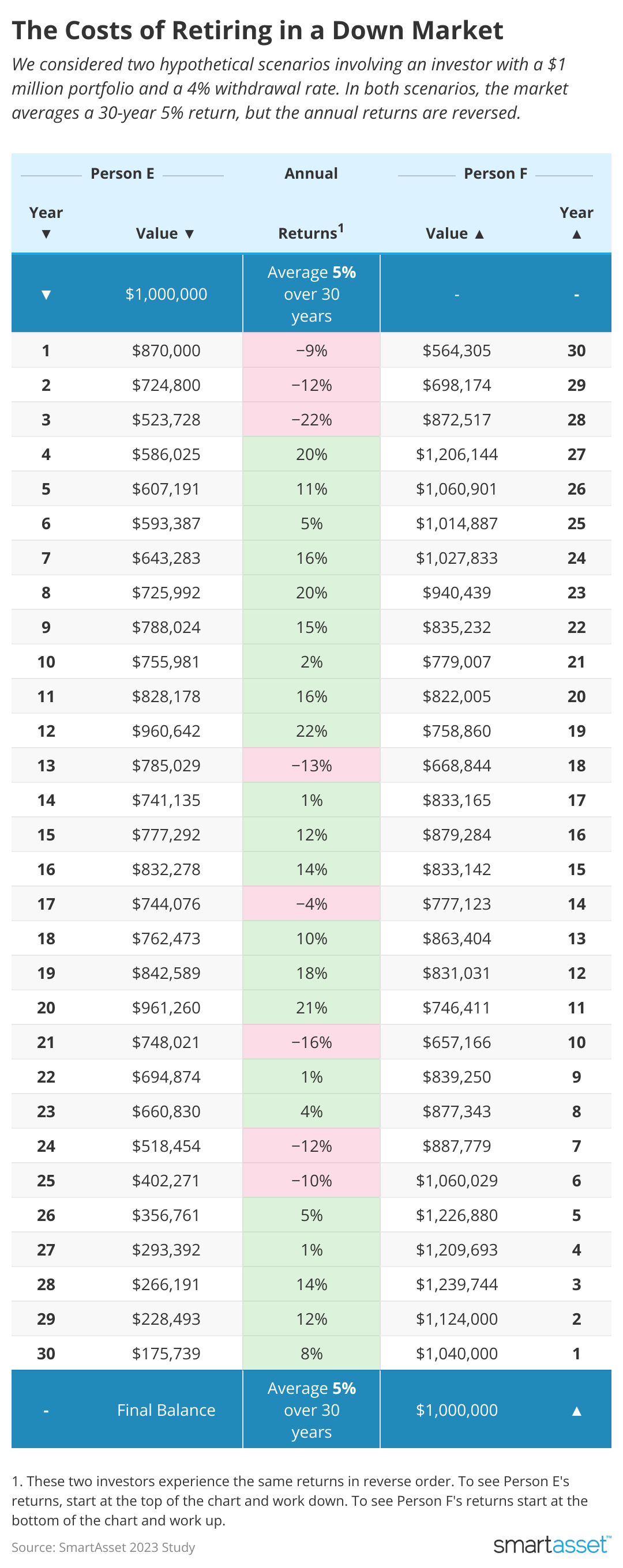

Another illustration of sequence risk

Here's one more chart that can show how important sequence risk is.

These numbers are just illustrative. Both accounts return 5% over 30 years. And both of them have the same annual returns. It's just that they're inverted. One retiree retires in an up year. The other retires in a down year. Look at the difference in their account sizes at the end of 30 years.

Bottom Line

Sequence risk matters. New or soon-to-be retirees considering drawing down investments should have a plan to prevent early market losses from doing long-term damage to their portfolios. Consider strategies to put off or reduce withdrawals, such as continuing to work or consult instead of retiring in a down market.

This story was produced by SmartAsset and reviewed and distributed by Stacker Media.