What credit score do I need for an auto loan?

There's no set minimum credit score required to get an auto loan. It's possible to get approved for an auto loan with just about any credit score, but the better your credit history, the bigger your chances of getting approved with favorable terms.

Experian compiled data on what you need to know about how your credit score affects a car loan, what credit score you need to get approved and other things to consider before applying.

What credit scores do auto lenders use?

The first thing you need to know about your credit score and auto loans is that auto lenders may use a different credit scoring model than you're used to seeing when you check your own credit.

Depending on the lender, they may use one of the following:

- FICO Scores 8 and 9: These two models are the latest versions of FICO's basic credit score. They provide a general look at your overall creditworthiness. You may have access to one of these scores through your credit card issuer or a credit monitoring service.

- FICO Auto Scores: FICO also provides credit scoring models that are specific to the auto industry, giving lenders more detailed information on your likelihood of paying back a car loan on time. If a lender uses this score during the underwriting process, any past payment issues you've had with auto loans could make it more difficult to get approved.

- VantageScore 3.0 or 4.0: These two models are provided by VantageScore, which was created by the three credit reporting agencies—Experian, Equifax and TransUnion. The VantageScore models have many small differences from the FICO models, but they use the same information (your credit report) to determine your creditworthiness.

Unfortunately, you don't have control over which credit score lenders use when evaluating your application. However, using your base FICO credit score can be a good indicator of your chances of approval.

The FICO Score ranges from 300 to 850 and is broken down into five tiers, or bands:

- Exceptional: 800-850

- Very good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

With good to exceptional credit, you have a good chance of getting approved by many auto lenders. If you have fair or poor credit, you may still be able to qualify for a loan, but lender options can be limited, and there may be other restrictions you have to deal with.

What credit score do I need for an auto loan?

There isn't one standard credit score required to qualify for an auto loan. Lenders look at your credit score when they review your application for a car loan, alongside other financial factors, such as your income.

Your credit score is an important factor in determining your ability to repay debt. But how it affects your auto loan can vary based on the lender you choose and the scoring model or models they use to evaluate your creditworthiness. In general, though, the higher your credit score, the better your chances of scoring a low interest rate and less restrictive loan terms.

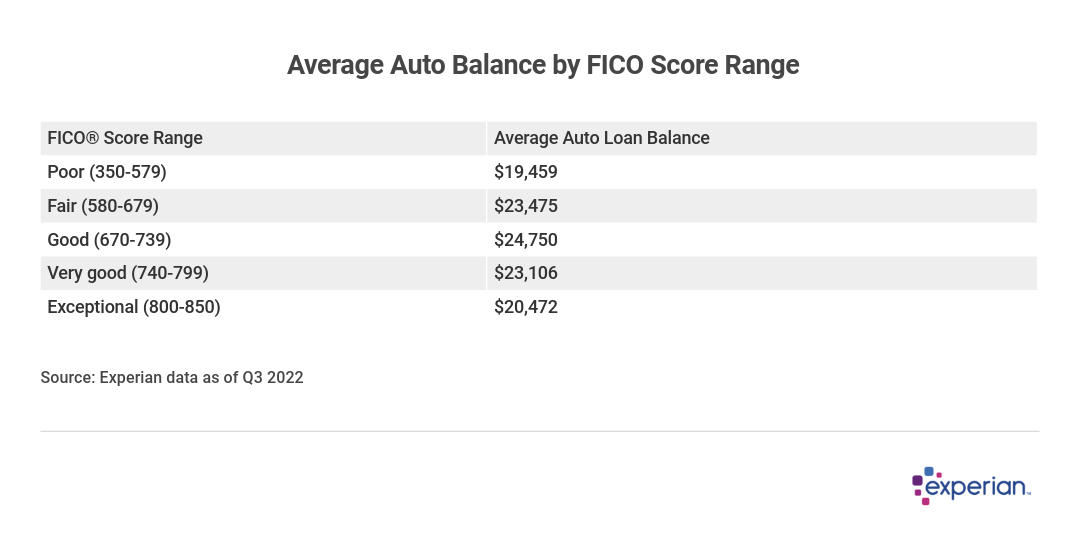

Although the average outstanding auto loan balances are roughly similar for borrowers no matter the score band, loan APRs vary widely based on the borrower's score. Those with higher scores are more likely to receive lower financing rates, which will allow them to get more for their money while paying less in interest.

Can you get an auto loan with bad credit?

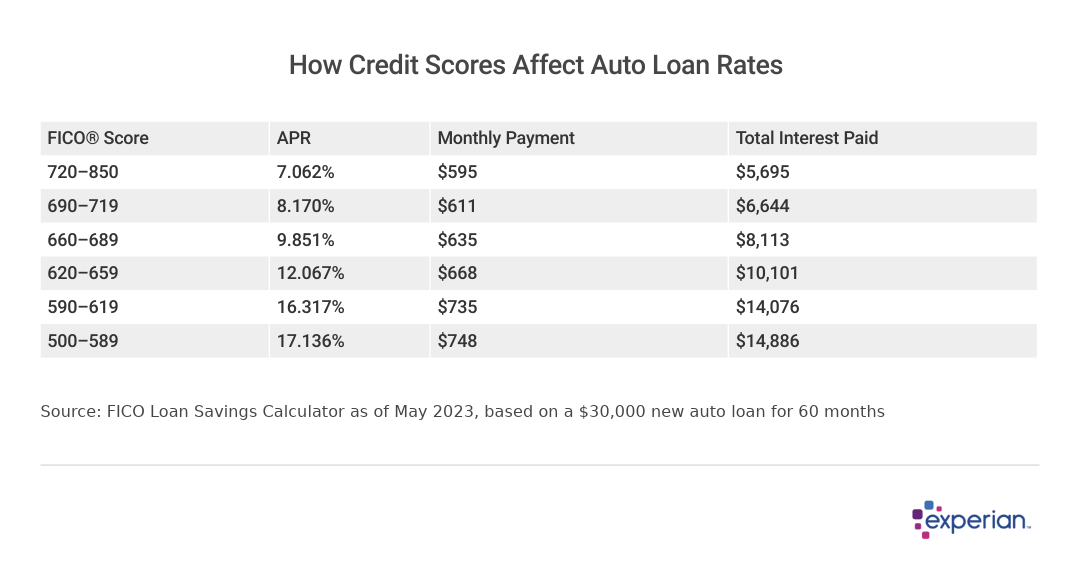

While it's possible to get an auto loan if your credit needs improvement, you probably won't qualify for the same terms as an applicant with a high credit score. That's because lenders view poor credit as a sign of risk, and charge higher interest accordingly.

For example, if you have a good credit score, you may be able to finance $30,000 for a new vehicle with a 7.06% APR over 60 months. In this scenario, your monthly payment would be $595, and you'd pay $5,695 in interest over the life of the loan.

If you have poor credit and your APR is 17.13% on that same amount, however, your monthly payment would jump to $748, and you'd pay $14,886 in interest over the 60-month term.

In other words, it is possible to get an auto loan regardless of your credit situation, but doing so with poor credit could cost you thousands of dollars, making it less appealing if you don't need a new car.

One thing to keep in mind, though, is that your credit score isn't the only factor lenders consider during the application process. They'll also look at your credit report, your debt-to-income ratio (DTI) (your monthly debt payments relative to your gross monthly income), your employment history and other factors.

If your credit score isn't in great shape but your financial profile is strong overall, it could potentially improve your chances of getting a lower interest rate.

How to apply for an auto loan

If you need a new car and need to get a car loan, there are a few things to do before you start the process.

1. Check your credit score

Check your credit score to understand your chances of getting approved with certain lenders and what loan terms and costs you can expect. If your credit score is in poor shape and you're not in a rush to buy a new car, consider working on improving it before you apply. Ways to build your credit include:

- Check your credit reports for errors and dispute them with the credit reporting agencies.

- Check your credit report for legitimate issues in your credit history that need to be addressed, such as late payments, collection accounts and high credit card balances.

- Get caught up on late payments, if applicable, and continue to pay your debts on time going forward.

- Keep your credit card balances low relative to their credit limits to improve your credit utilization rate.

- Limit how often you apply for new credit to only when you really need it.

If you have bad credit and need a car now, getting a cosigner, making a large down payment and looking for a second-chance car loan can help improve your chances of getting financing.

2. Research lenders

Shopping around is one of the best things you can do to save money on your car loan. Different lenders have varying eligibility criteria and terms, so by comparing multiple lenders, you'll have a better chance of finding the loan that's the best fit for you and costs the least.

3. Have a good down payment or trade-in

Putting money down or trading in a car on your loan can reduce how much you borrow, saving you money on interest charges over the life of the loan. Depending on the situation, it could also lower your interest rate because the lender is taking on less risk with a smaller loan.

It can take time to save money for a down payment, so start sooner than later. And keep in mind that selling a car to a private party could net you more cash than a trade-in, so if that's possible, opt for that instead.

4. Get preapproved before you buy

Many banks and other auto lenders allow borrowers to get preapproved before they ever step foot in a dealership. This process doesn't take long—you can often do it online—and it can allow you to potentially get financing for less than what the dealer can arrange with its partner lenders.

5. Build credit for lower rates

The key to qualifying for a better auto loan rate is to start improving your credit well before you need to apply. To avoid getting caught with a high-interest loan, work on practicing good credit behavior all the time. Not only will it help you score a better auto loan, but it can also reduce how much you pay for other types of credit, lower your auto and homeowners insurance rates, and have many other positive effects.

This story was produced by Experian and reviewed and distributed by Stacker Media.