Secure 2.0: How super-catch-up contributions can grow your retirement

Secure 2.0: How super-catch-up contributions can grow your retirement

Catch-up contributions allow people age 50 and older to save extra money in their retirement accounts. These additional savings are currently capped at $7,500 per year, but some workers will soon be eligible to save more money for retirement thanks to the SECURE 2.0 Act.

Starting in 2025, people ages 60 to 63 can save an extra $10,000 in their 401(k), or 150% of the standard catch-up contribution limit per year, whichever is greater.

SmartAsset crunched the numbers to see just how big of an impact the enhanced catch-up contributions can have on a person's retirement outlook. The extra savings may not seem like much in the short term, but those dollars can grow substantially over the course of a decades-long retirement.

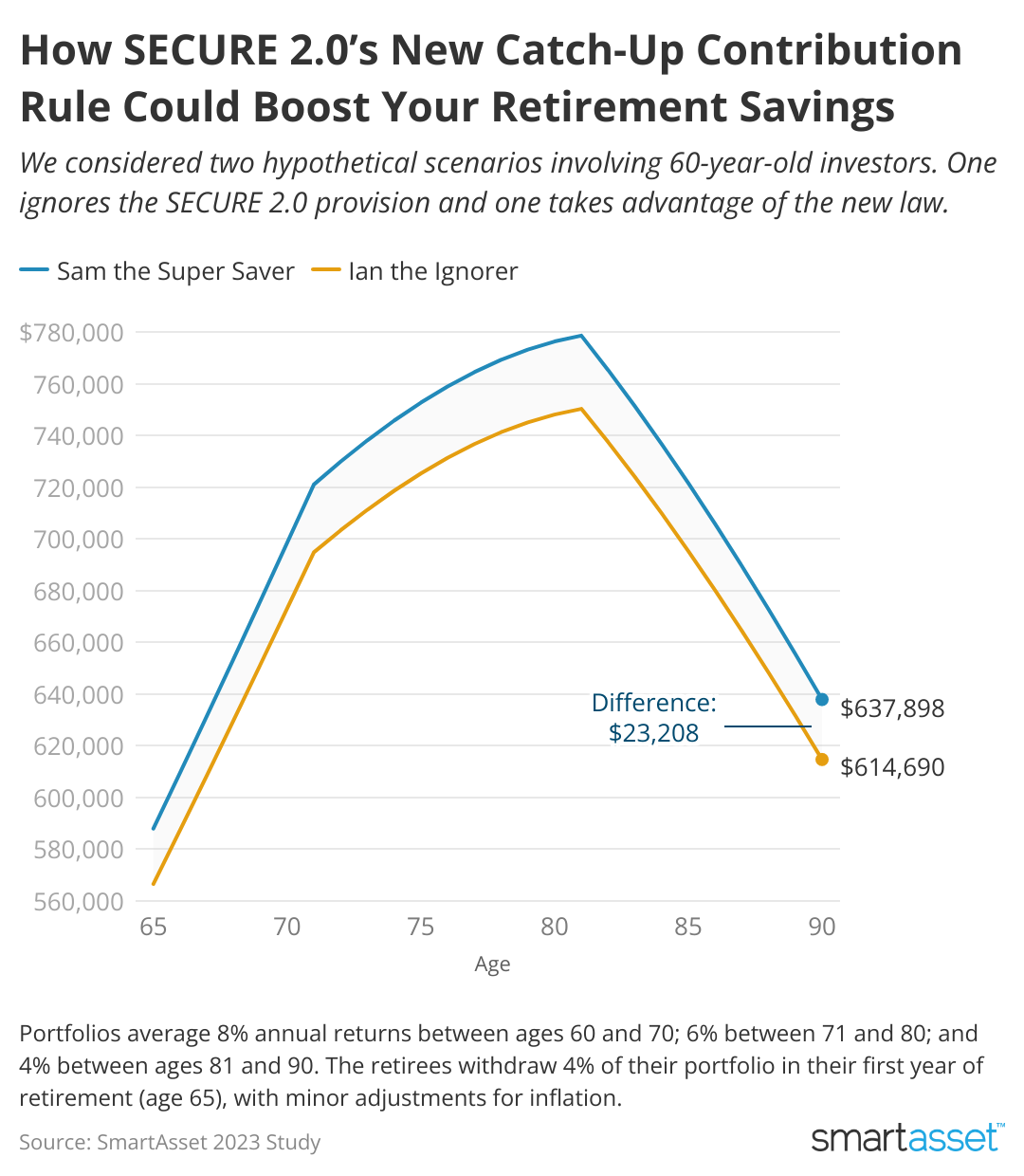

Ian the Ignorer vs. Sam the Super Saver

Imagine two 60-year-olds who plan to retire at age 65. Both have $256,244 already saved in their 401(k)s – the average defined-contribution plan balance for people ages 55 to 64, according to Vanguard. Both people can also afford to max out their 401(k)s each year and add another $7,500 in catch-up contributions.

One of them, however, takes advantage of the SECURE 2.0 provision and saves even more during the four-year window when enhanced catch-up contributions are allowed. The other ignores the provision.

Here's a closer look at how much the two people contribute to their 401(k)s:

Ian the Ignorer: Ian ignores the new law and continues to save $22,500 in his 401(k), plus the $7,500 catch-up contribution. As a result, he saves $30,000 a year throughout his early 60s.

Sam the Super Saver: Sam, on the other hand, takes advantage of the new law. From ages 60 to 63, she fully maxes out her 401(k) by contributing $22,500, plus the enhanced catch-up contribution.

In her first year of eligibility, the bonus catch-up is worth $11,250 (150% of $7,500). Because the limit will increase annually with inflation, Sam is able to make a slightly larger catch-up contribution (the study assumed a 2% increase) every year until age 64. At that point, she's no longer eligible for the SECURE 2.0 bonus but she resumes making the regular $7,500 catch-up contribution.

Let's compare: How enhanced catch-up contributions impact portfolio returns

Between ages 60 and 64, Sam saves $166,369 compared to Ian's $150,000. But that's not the end of the story. Assuming Sam and Ian each live into their 90s, their money will remain invested for decades and continue to grow based on the following assumptions:

- Asset allocation. The two savers invest their money in identical portfolios. Their asset allocations get increasingly conservative as they age.

- Annual investment returns. Because their portfolios are identical, Ian and Sam see the same investment returns each year. Their portfolios average 8% per year between ages 60 and 70; 6% between ages 71 and 80; and 4% between ages 81 and 90. These returns are illustrative to reflect a ratcheting down of investment risk as Ian and Sam age.

- Annual withdrawal rate. Both Ian and Sam withdraw 4% of their portfolio in their first year of retirement (age 65), with minor adjustments for inflation.

By the time Ian is 90 years old, he'll still have nearly $614,690 – despite making regular withdrawals from his portfolio each year.

As for Sam, the larger catch-up contributions mean she'll start retirement with $16,000 more than Ian. But as the years go by, the difference between Sam's and Ian's savings grows even larger. By her 90th birthday, Sam's portfolio is worth $637,898 – $23,208 more than Ian's.

Bottom line

As retirement approaches, catch-up contributions can help you supercharge your 401(k) and reach your savings goal. Starting in 2025, the SECURE 2.0 Act will allow people ages 60 to 63 save even more via an enhanced catch-up contribution. Those extra dollars can add up over the course of a 25-year retirement and continue to compound along with retirement account investment growth. However, the potential long-term growth of those enhanced contributions simply may not be enough to entice some pre-retirees to save the extra money between ages 60 and 63.

This story was produced by SmartAsset and reviewed and distributed by Stacker Media.